Authors: Ben Wilson, Travis Lucas, Miles Forsyth-Hecken

Published: April 2026

Efficiency is the foundation of a well-run railway. Positive passenger outcomes, reliability and value for money are all determined, in part, by the extent to which the railway is operated efficiently. Hence, enhancing efficiency is not just an operational goal, but a prerequisite for achieving better outcomes.

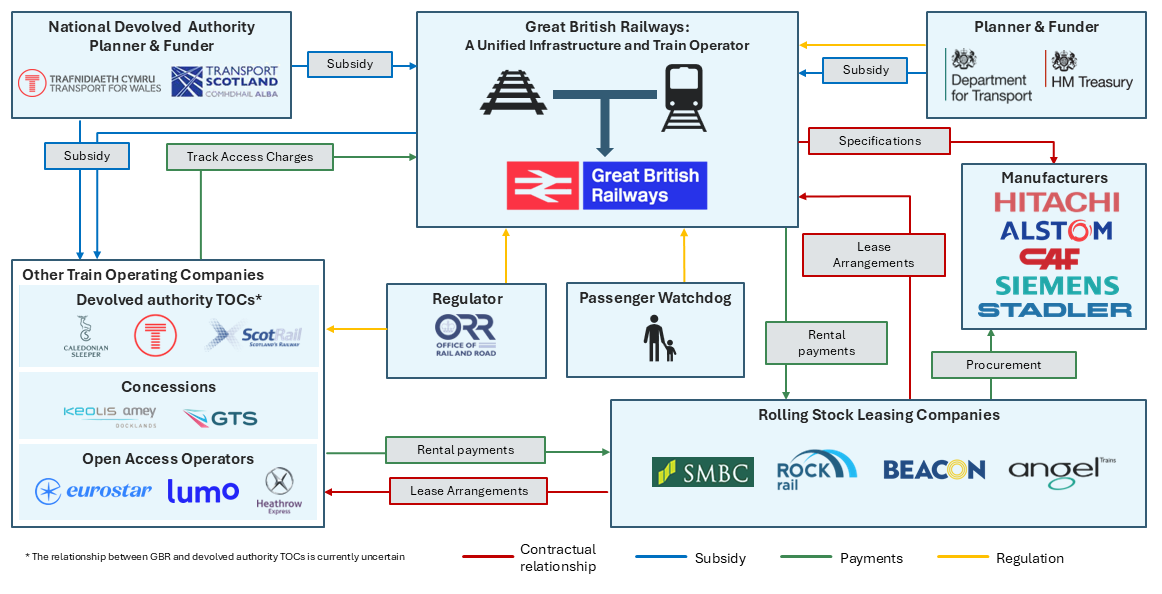

In light of ongoing concerns about the efficiency of rail operations in the UK, underpinned by poor punctuality, ticket unaffordability, and inefficient operational structures, the government launched a plan for industry reform in 2021 which has evolved into the current vision for Great British Railways (GBR). GBR will be a single publicly owned entity that consolidates operations and infrastructure management as a “directing mind”. The full-scale launch of GBR is imminent with the Railways Bill entering parliament in late 2025 and train operating companies (TOCs) being brought into public ownership through 2027[1].

The current trajectory of UK rail policy focuses on GBR’s structure and unlocking efficiencies through getting this structure ‘right’. However, important non-GBR stakeholders will still exist after industry consolidation is complete, including devolved governments, rolling stock manufacturers, and rolling stock leasing companies.

Rolling stock leasing companies are critical stakeholders, supplying nearly all the UK’s rolling stock. The government has signalled rolling stock, and by extension the leasing companies, will remain in the private sector, citing the immense amount of capital that would be required to acquire rolling stock assets[2]. We believe the leasing business model adds value to the industry by enabling risk transfer, as well as bringing expertise in asset management and procurement. Put together, the comparative advantage of leasing companies results in greater investment and more efficient delivery, improving outcomes for passengers sooner than if we relied on public finance.

Figure 1: The future UK rail industry structure with Great British Railways will create decidedly different market dynamics

While the position of leasing companies will remain unchanged, market dynamics will be decidedly different with a single operator and lessee (i.e. GBR) replacing the rail franchising system. Whether this new industry structure succeeds in driving efficiencies in rolling stock financing and procurement largely depends on how the new partnership is defined and maintained.

In this paper, we identify three conditions that must underpin a successful partnership between GBR and leasing companies. These comprise:

- Standardisation (spanning technical, procurement, and contractual standards)

- A committed programme

- Effective risk allocation

Satisfying these conditions will build on the leasing companies’ value proposition and unlock further value for the industry. With a strengthened partnership, leasing companies will be enabled to respond more readily and align more closely to the strategic direction set by GBR.

Standardisation

Under the previous franchising system, rolling stock was procured by multiple bodies, each operating to their own timescales, specifications and commercial processes. With GBR, the industry will have a single lessee with sufficient scale and authority to drive standardisation across the industry. In this context, three distinct opportunities arise from standardisation. First, technical standardisation, where GBR can work with manufacturers to develop standardised rolling stock platforms. Second, procurement standardisation, where GBR can develop a consistent approach to bid requirements, evaluation and asset management. Third, contract standardisation, where a common suite of model contracts can streamline legal and administrative processes.

Taken together, standardisation can materially enhance efficiency across the railway. The challenge will be to secure these benefits while retaining sufficient flexibility to provide for different service needs as well as competition in the market.

Technical standardisation

Under the new centralised GBR structure, procurement can take place at a portfolio level rather than through individual operator-led competitions. As a result, there is an opportunity to realise economies of scale for manufacturers who develop standardised and modular rolling stock platforms.

While there is no formal standardisation at present, rolling stock standards have already tended towards an implicit industry standard. The development of modular product platforms such as Aventra and Desiro City have demonstrated that standardisation can deliver scale and cost efficiencies[3]. Under a more consistent national framework, GBR could strengthen these benefits. With clearer visibility of future portfolio wide needs, manufacturers could plan investment with greater confidence, reducing bespoke engineering, lowering production risk and improving whole life value.

The deciding factor for these benefits will be whether standard platforms can retain the adaptability required for different operational contexts, from intensive commuter routes to regional services. Too prescriptive of an approach risks imposing uniformity where variation is needed; for example, in Germany, the TALENT platform suffered from limited flexibility beyond its base offering and consequently saw limited orders outside Germany[4]. There is also the risk of limiting competition and innovation if standards become too specific. To mitigate this, the standards should be based on principles and outcomes, not prescriptive technical requirements.

Figure 2: The Bombardier Talent 2 Platform highlights the drawbacks of a one-size-fits-all approach

The onus is therefore on GBR as the client to ensure they have the capability to understand what is required and define standards that support scale, reliability and innovation. To achieve this, GBR must work closely with manufacturers and leasing companies from the outset to gather expert views and find the right balance between standardisation and flexibility.

Procurement standardisation

GBR can deploy its directing mind to provide a standardised process for commercial procurement, evaluation and asset management. By delivering a common process with familiar proposal requirements and evaluation approaches, private sector suppliers can develop better bids with more consistency and at a lower cost.

Historically, each procurement competition has its own bid requirements, evaluation criteria and asset management expectations, resulting in a patchwork of approaches that increased the cost and complexity of bidding. While it may be fair to say that since the Thameslink Programme procurement the general approach has remained consistent, the details have remained quite varied. Removing this variation through a consistent set of processes would enable suppliers to prepare higher quality, more comparable bids and reduce delays caused by the repeated reinvention of commercial frameworks. There is also little risk involved in introducing such practices, as the market has signalled that it would welcome a standardised process which is reliable and easy to navigate.

However, it will be challenging to develop a process that is sufficiently familiar to the market but allows procurement teams to tailor in accordance with their needs. Some tailoring and re-weighting will always be necessary. Therefore, the aim should be establishing a familiar baseline with clear templates, consistent evaluation methodologies and predictable information requirements, that procurement teams can build upon.

Contract standardisation

Efficiencies are to be gained from establishing a common set of model contracts to facilitate the procurement of rolling stock. Currently, there is a wide array of different model contracts used in rolling stock procurement. They all cover the same issues and look very similar; informally they have tended towards standardisation. GBR as the centralised lessee of rolling stock will have the opportunity to establish a common set of model contracts and formally standardise the process.

The informal standardisation which has already occurred means the time and procurement cost savings created from further standardisation at the GBR level will be limited. However, the real benefit of contract standardisation will come from a common set of acceptance requirements, payment terms, liquidated damages regimes, liability caps, and responsibility allocations. Familiarity with these standards will reduce uncertainty and risk for suppliers, saving time and cost by enabling more efficient pricing.

Committed programme

The second condition is whether GBR can provide leasing companies and the industry supply chain with a clear committed programme. It is well understood that better information and confidence in upcoming demand is an enabler of efficiency in any industry. However, it is particularly relevant to the UK railways, where long asset lives, specialist skills and capital-intensive manufacturing leave the market vulnerable to fluctuations in demand.

Historically, the UK has struggled to provide a high level of certainty in rolling stock procurements. Programmes have often been fragmented, reactive and subject to political cycles which leave manufacturers, funders, and leasing companies without the visibility needed prepare for future requirements. Not only has this limited the resilience and responsiveness of the supply chain in the short term, but it has also created structural constraints for delivering in the longer term[5].

As the industry’s directing mind, GBR will be positioned to take a network-wide view of rolling stock requirements and signal its intentions with greater certainty. GBR could design a coherent national programme, sequencing procurements, align renewal cycles and communicating a clear forward view to leasing companies and manufacturers. In doing so, GBR should learn from recent challenges and establish a strong governance structure that can mitigate disruptions.

There is also international precedent to draw upon. Several European governments publish codified, regularly updated pipelines or target-timetable programmes which investors regard as bankable signals. For example, the Netherlands provides an annual, parliamentary-tabled, multi-year project list with status and planning milestones, giving suppliers and financiers predictable visibility[6].

Risk allocation

Finally, arguably the most decisive condition underpinning an effective partnership between GBR and rolling stock leasing companies is risk allocation. In capital-intensive procurements such as rolling stock, the distribution of risk directly shapes the propensity to invest, the cost of capital, and by extension, the overall value delivered to taxpayers. Private capital is acutely sensitive to risk transfer; when too much risk is transferred to investors, pricing escalates, or investment withdraws altogether. Conversely, when too little risk is transferred, the public sector shoulders too much exposure, weakening accountability and undermining value for money. The challenge therefore is to strike a balance that aligns incentives without deterring participation.

The Class 365 procurement highlights how misaligned risk allocation can distort long‑term value. The decision to lease the fleet resulted in transferring significant financial and residual‑value risk to private lessors, which later constrained redeployment and increased whole‑life costs. The Thameslink and Intercity Express Programme procurements offer further examples where unclear or poorly balanced risk allocation can lead to delays, higher costs, and reduced value for money[7] in an environment where the base product was of a high quality.

Figure 3: The procurement of Class 365 rolling stock highlights where insufficient risk was transferred to private lessors

GBR will have the opportunity to address these past shortcomings. A clearer, more consistent approach to risk allocation – embedded within standardised contracts, transparent procurement processes, and early engagement with leasing companies – can ensure that risks sit with the party best placed to manage them. This will improve accountability, lower financing costs, and encourage sustained investment across the supply chain.

Ultimately, risk allocation is not a technical afterthought but a strategic determinant of whether GBR’s partnership with the private sector will succeed. Getting it right will foster a more stable financial environment. Getting it wrong risks repeating known failures of the past.

A more efficient railway means better outcomes for all

A more efficient railway is the common foundation on which both GBR and rolling stock leasing companies can meet their strategic objectives. For leasing companies, efficiency lowers costs, reduces risk, and shortens timelines. For GBR, it enables reliable services, affordable fares, and stable demand. Each depends on the other, with GBR needing sustained private investment and investors needing clear policy and predictable passenger demand.

Delivering the three conditions set out in this paper, standardisation, a committed programme and balanced risk allocation, turns that alignment into action. The private sector will welcome a clear and consistent framework because it supports sharper pricing, faster mobilisation and resilient supply chains. Conversely, if GBR does not provide this clarity from day one, procurement will drift, costs will rise and investment appetite will narrow, weakening outcomes for passengers and taxpayers. Commit to these conditions with discipline and flexibility, and the result will be a railway that is more reliable, more affordable and better for all.

Looking further ahead

As partnerships in the industry mature, there will be further opportunities to unlock efficiencies and strengthen collaboration. We have identified the following areas for further consideration as the industry continues to evolve:

- Clarifying roles and responsibilities across DfT, GBR, DFTO and rolling stock leasing companies – examining how partnerships between these organisations should operate in practice, beyond the high‑level public–private distinction. This includes understanding how DfT policy will influence decisions such as risk allocation and long‑term investment planning.

- Defining GBR’s ‘market‑shaping’ role – articulating how GBR should set strategic direction, coordinate diverse stakeholder interests and guide the market in a way that supports resilience, innovation and value for money.

- Exploring opportunities for greater involvement from rolling stock leasing companies following track–train integration – assessing how leasing companies could contribute more actively to system delivery. This could range from major shifts, such as providing integrated procurement solutions for both track and train, to more incremental changes including collaborative planning. Hybrid models may also emerge, for example leasing companies supplying supporting infrastructure such as depots, batteries or monitoring systems.

- Increasing contributions from rolling stock leasing companies to whole‑system thinking – considering how leasing companies could support the development of national fleet strategy and wider system optimisation. As trust and partnership deepen, bringing broader perspectives into long‑term planning becomes more valuable. However, any expansion of this role must be balanced carefully to avoid raising barriers to entry or creating conflicts of interest.

[2] Rolling Stock: Purchasing Models – Hansard – UK Parliament

[3] Procuring new trains – NAO report

[4] There were a small number of deployments in other European countries (largely Austria) but were very limited compared to the volume of orders in Germany.